Modern Prop Trading — Since 2015

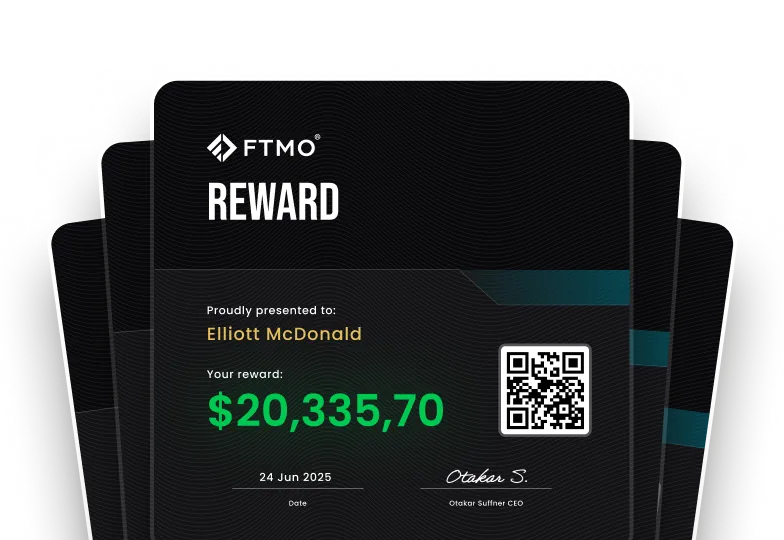

Grow & Monetize

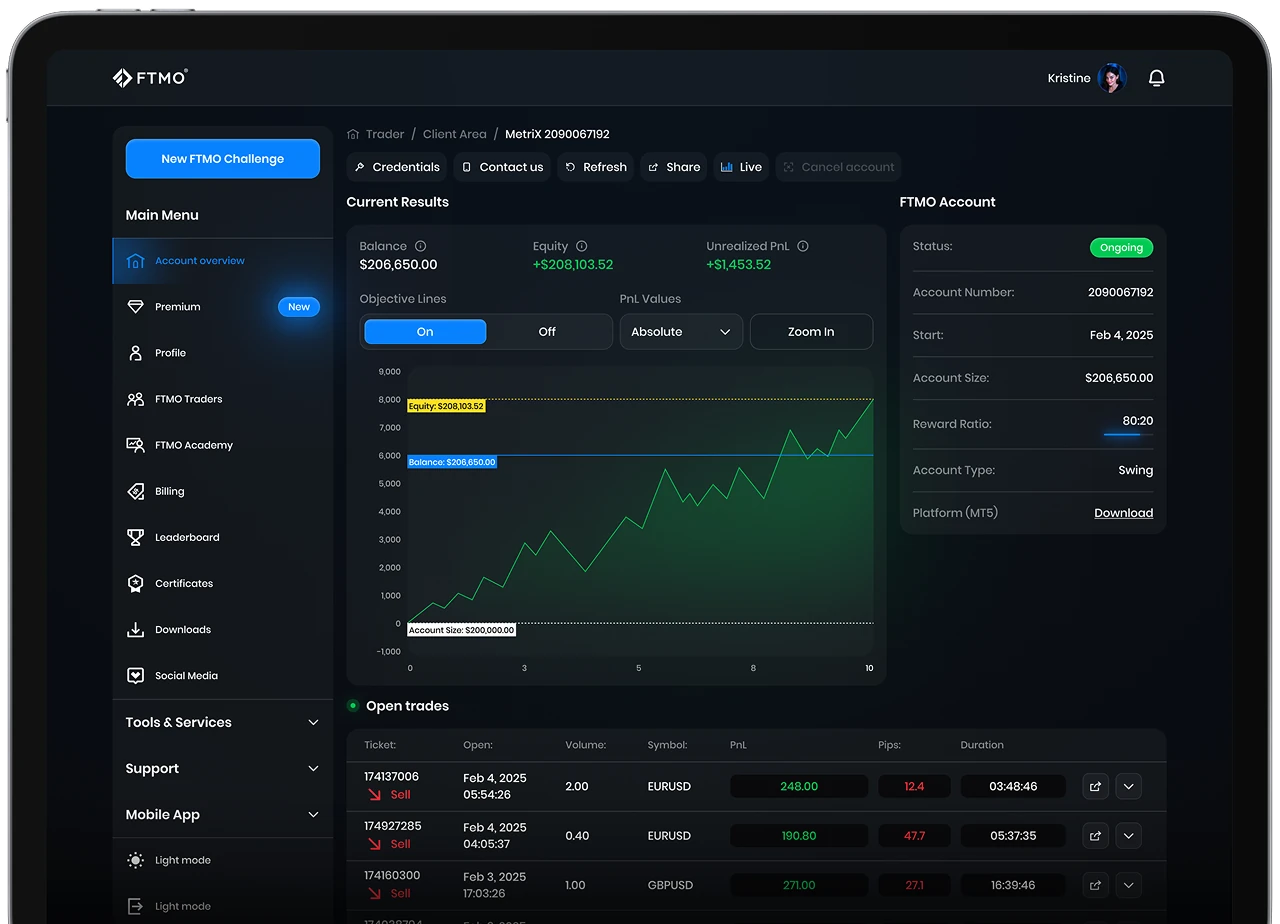

Your Demo Trading

Improve your trading skills on our simulated platform and earn rewards

- Up to $200,000 FTMO Account

- Support in 20 Languages

- 3 Trading Platforms